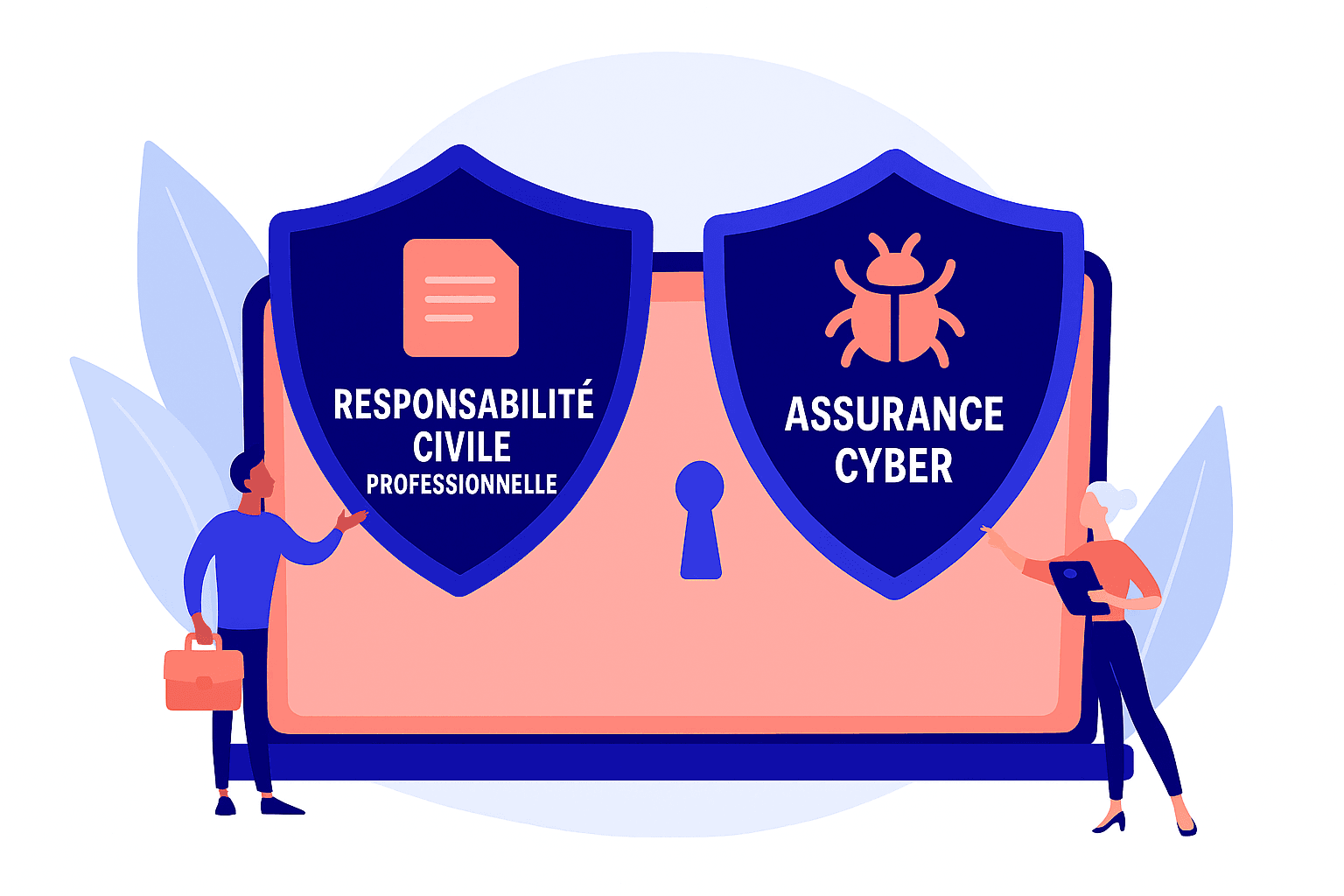

Professional liability and cyber insurance: coverage with very different objectives

Professional indemnity (RC Pro) is a well-known form of cover for businesses. It covers damage caused to third parties (customers, partners, suppliers) as a result of fault, error, negligence or lack of advice in the course of professional activity.

> For example, a web agency forgets to renew a customer's domain name, resulting in lost sales. Pro Liability may be called in to compensate the customer.

Cyber insurance, on the other hand, covers events of IT origin: ransomware, theft or loss of data, compromise of an information system, phishing, and so on.

It has two components: - the insured company's own losses (business interruption, restoration costs, crisis communication...) - its liability towards third parties indirectly affected by the cyber attack.

> Example: a company suffers a leak of customer data. If this data is sensitive (e.g. health, finance), it may be held liable for inadequate protection.

What changes: the origin of the loss

The major difference between professional liability and cyber insurance is the origin of the loss.

- If the problem stems from human error or bad advice, you're covered by professional liability.

- If the problem stems from an attack or computer flaw:cyber insurance takes over.

The risk? Liability and cyber insurers passing the buck, each believing it's not their place to intervene. The result: grey areas, delays, and sometimes... no compensation at all.

Pitfalls to avoid: high deductibles, cross exclusions, sub-limits

When taking out a policy, you need to pay particular attention to :

- ✅ The deductible level: too high a deductible can render insurance useless in the event of a low-intensity claim.

- ✅ Cross exclusions between RC Pro and cyber: some clauses may exclude claims that fall partially under both coverages.

- ✅ S ub-limits, notably on data theft, betterment (technical upgrading), or contractual penalties imposed by a customer.

These limits are often difficult to read and a source of confusion. Hence the importance of a well-designed contract.

Professional liability + Cyber: an essential combination

At Dattak, we believe in simple, clear and comprehensive protection. That's why we've launched a combined RC Pro + cyber insurance policy.

A 360° policy:

- Covers malpracticeand cyber attacks - Avoids thegrey areas between two separate policies - Draws on the best of our two areas of expertise (liability and cyber) - Enablesrapid coverage, with no conflict of interpretation> In short: greater clarity, less stress for the insured... and protection that can be activated when it counts.

In conclusion

Professional liability and cyber insurance don't play the same role, but together they're essential.

In a world where the line between human error and computer attack is becoming blurred (e.g.: an employee clicks on a phishing link), it's crucial to anticipate how the two types of cover should interact.

The combined policy offered by Dattak is designed to respond to this reality: a single policy, comprehensive coverage, zero unpleasant surprises.

💡 Want to find out more? Contact our teams or discover our combined offer on our website. Cyber risk is the number 1 risk for any business, whatever its size.